Can a Collection Prevent Me from Getting a Mortgage?

Learn how collections on the credit report can affect you and possible ways to handle them.

Applying for a mortgage is one of the most significant financial steps many people take in their lives. It is a process that involves more than just demonstrating an ability to make monthly payments. It requires a detailed review of your entire financial picture including your credit history. One element that often causes concern for potential homebuyers is the presence of a collection or multiple collections on their credit report. Whether its an old utility bill, a medical bill or a forgotten credit card payment, collections can leave borrowers wondering whether they will be disqualified from securing a home loan.

This leads to the question, "Can a collection prevent you from getting a mortgage?" The short answer is it depends. Collections do not always mean a mortgage is out of reach, but it can add an extra item to deal with. How much they impact your application depends on several factors including the type of collection, its age, the size of the debt, and the type of mortgage you are applying for.

Understanding What a Collection Means

When a creditor sends an unpaid account to a collections agency, it typically means the original lender has written off the debt as a loss. That action is then reported to the credit bureaus, and it becomes part of your credit file. Collections can remain on your report for up to seven years, and during that time, they can have a damaging effect on your credit score.

Mortgage lenders look closely at your credit report as a way of gauging risk. A collection account signals that at some point, you failed to meet a financial obligation. Even if the account has been paid off or settled, it still tells a story of missed payments and possible financial instability. However, not all collections are treated equally.

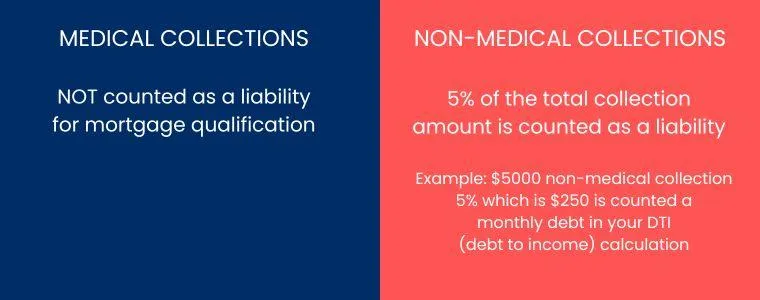

Medical vs. Non-Medical Collections

Recent changes in the credit reporting landscape have shifted how medical debt is handled. Many underwriters, particularly those reviewing guidelines for Fannie Mae or Freddie Mac, have started to look more leniently at medical collections. Some versions of credit scoring models even exclude paid medical collections altogether. This shift reflects the growing recognition that medical debt often arises from emergencies rather than poor financial planning.

Non-medical collections, on the other hand such as those related to credit cards, personal loans, or utility bills tend to carry more weight in a lender’s decision. These are typically seen as stronger indicators of financial management and reliability. A history of non-medical collections, especially recent or unpaid ones, can raise red flags.

If an individual has one or several collections, underwriting will usually count 5% of the total collection amount. For example, if there is a $1000 utility collection, 5% is $50 per month accounted as a liability; if there is a $2000 collection for a personal loan which was not paid, 5% of the amount is $100, and this would be counted as a monthly debt; $5000 open collection for a car loan which was not paid translates into $250 per month as a monthly debt which is counted as a liability.

In some cases, the amount is rather small and if the credit is overall reasonable, this may not have a big impact. On the other hand, if the credit was mediocre to begin with, and then add in a few collections, the score can drop and these monthly debts that have to factored in could require some resolution before proceeding.

When it's a medical bill, the calculation used above would usually not be applicable. The underwriter will see the collection, but will not count against the borrower who is trying to purchase or refinance the home. But, keep in mind, that if the credit was mediocre or poor to begin with, having the medical collections can lower the scores further and create other obstacles that have to be reviewed beforehand.

How Collections Affect Mortgage Approval

The impact of a collection on your mortgage approval will also depend on the type of loan you’re applying for. Government-backed loans such as FHA, VA, and USDA loans often have different guidelines than conventional mortgages.

For example, FHA loans allow for certain collections, especially if the total outstanding balance is below a specific threshold. However, if the cumulative balance of all non-medical collections is above that threshold, a mortgage underwriter may require the debt to be paid off or documented before closing. VA loans tend to be more flexible focusing more on your overall ability to repay the loan rather than rigid rules about past collections. Conventional loans, which are not backed by a government agency, often have stricter credit requirements. A recent collection account, even if it has a small balance, might lead a lender to deny the application or offer less favorable terms.

Another aspect lenders consider is whether the collection account is paid or unpaid. While having a paid collection doesn’t completely erase its impact, it does show initiative and responsibility, which can help strengthen your application. An unpaid collection, especially if it's recent or significant in size, poses a greater risk to lenders and could prevent approval entirely.

Credit Scores and Collections

Your credit score plays a central role in mortgage qualification. Collections typically lower your score, and the drop can be substantial depending on how recent the collection is and how much was owed. Most lenders have minimum credit score requirements, and if a collection has dragged your score below that threshold, you may need to take steps to repair your credit before applying.

It’s worth noting that not all lenders use the same credit scoring model. Some may use newer models that weigh collections differently, particularly those that de-emphasize or exclude paid medical debts. Even in those cases, an underwriter may still look at the full credit report during manual underwriting, and the presence of collections will still be visible.

Steps You Can Take in Preparation of Obtaining a Mortgage

If you are worried about a collection on your credit report and how it might affect your chances of getting a mortgage, there are several things you can do to prepare. First, obtain a copy of your credit report and review it carefully. Look for errors or outdated information. Collection accounts that have aged beyond the reporting limit should no longer appear. If you spot inaccuracies, dispute them with the credit bureau.

If the collections are valid, consider paying them off, especially if they are recent or relatively small. In some cases, you may be able to negotiate a “pay for delete” agreement with the collection agency in which they agree to remove the account from your credit report in exchange for payment. While not all creditors offer this, it can certainly be worth asking.

You might also consider speaking with an experience mortgage broker before applying. Our team can help you understand how your specific credit profile will be viewed by an underwriter and offer advice on whether paying off certain debts would improve your chances. In some cases, waiting a few months and focusing on improving your credit may be the most strategic path to homeownership.

A collection on your credit report doesn’t automatically prevent you from getting a mortgage, but it does make the process more challenging. An underwriter wants to see that you are financially responsible and capable of managing debt. While one or two older, paid-off collections might not be a deal-breaker, having multiple recent unpaid accounts could signal too much risk.

Ultimately, the best course of action is to be proactive. Understanding what’s on your credit report, taking steps to address any outstanding debts, and working with mortgage professionals who can guide you through the process will put you in a stronger position to secure the financing you need. With the right preparation, a collection does not have to be the end of your homeownership dream. It can simply be a hurdle to overcome.

For more information on a possible collection, or known collections, on your credit report and how to handle them, please contact us. We will be happy to assist you.

Mortgage Insight:

Purchasing a Home with a Conventional Loan

VA Loan Success Story with Eric and Denise

How a VA Loan in Ocala, FL changed a Family's Financial Future

How Much Home Can I Afford with a VA Loan?

Can I Use My VA Loan in a Chapter 13 Bankruptcy?

Can a Fiance or Kids be on a VA Loan?

Veterans Who Buy Homes See Far Higher Net Worth Than Renters

How Much Mortgage Insurance Can I Save with a VA Loan?

What to Avoid in a Home When Obtaining a VA Loan Appraisal?

Duplex Property in Fort Lauderdale Quadruples in Value and Leaves a Nest Egg to the Heirs

How a California Remote Worker Obtained a Mortgage to Relocate to Boca Raton, FL

What's the Average Mortgage in Fort Lauderdale, FL?

What Factors are in my Credit Score for a Mortgage?

What Documents Do You Need for a No Income Verification Mortgage?

Restaurant Owner Obtains Self-Employed Home Loan

Can a General Contractor Obtain a No Income Verification Mortgage?

Is a HELOC or a Cash Out Refinance Better to Pay for a New Roof?

Can a Collection Prevent Me from Getting a Mortgage?

Do I Have to Make Mortgage Payments if I Lose My Job?

Your mortgage journey.

Various loan type options including:

Conventional loan

FHA loan

VA loan

Self-employed loan options

No income verification for investors

Benefits of Homeownership

Homeownership is a significant milestone and a decision that offers many advantages. In addition to providing a place to call your own, owning a home brings financial stability, personal fulfillment, and a sense of belonging. Mortgage Group has been helping individuals and families obtain homeownership, guiding them through the process and obtaining referrals to help their family and friends accomplish the same.

Purchase

Get pre-approved to purchase your first home, second home or upcoming investment property.

Refinance

Own a property and interested in lowering your payment? Need to take cash out? Refinance with confidence.

Connect with Us

Our experienced team with be happy to speak with you, and walk you through each step of the process.

Providing mortgage solutions to help you with your home.

Mortgages can be complicated and have many moving parts. Let our team help you!

Contact Us

It only takes a few moments to reach out and have an initial conversation.

Know the Next Steps

Our team will work with you to find the best way to achieve your home loan goals.

Find Your Home and Get Your Loan

Our team will be prepared to move with the next steps once you have secured your home purchase contract.

Houses

Townhomes

Condos

Multi-Units

Contact our team today.

1-800-583-5305

© Copyright 2026 E Mortgage Capital, Inc.. All rights reserved.

- 1416824 | E Mortgage Capital, Inc.

Notice To Texas Loan Applicants: Consumers wishing to file a complaint against a mortgage banker, or a licensed mortgage banker residential mortgage loan originator, should complete and send a complaint form to the Texas Department of Savings and Mortgage Lending, 2601 North Lamar, Suite 201, Austin, TX 78705. Complaint forms and instructions may be obtained from the department’s website at www.sml.texas.gov

A toll-free consumer hotline is available at 1-877-276-5550. The department maintains a recovery fund to make payments of certain actual out of pocket damages sustained by borrowers caused by acts of licensed mortgage banker residential mortgage loan originators. A written application for reimbursement from the recovery fund must be filed with and investigated by the department prior to the payment of a claim. For more information about the recovery fund, please consult the department’s website at

www.sml.texas.gov