The Hidden Savings Veterans Unlock with VA Loans

See How Much Mortgage Insurance Veterans Can Save with a VA Loan?

For many veterans, the decision to buy a home is one of the biggest financial steps taken after military service. What some prospective homebuyers and existing homeowners don’t realize is just how powerful their VA loan benefit can be in making that step more affordable. In addition to benefits at the closing table, there are savings every single month when a payment is made towards the mortgage balance on a VA loan.

At the heart of the savings is one line item that most civilian borrowers can’t escape which is mortgage insurance. For those using a conventional loan with less than twenty percent down, private mortgage insurance (PMI) is usually required. On FHA loans, it comes in the form of a mortgage insurance premium (MIP). Either way, it’s a significant extra cost—often several hundred dollars tacked onto the monthly payment.

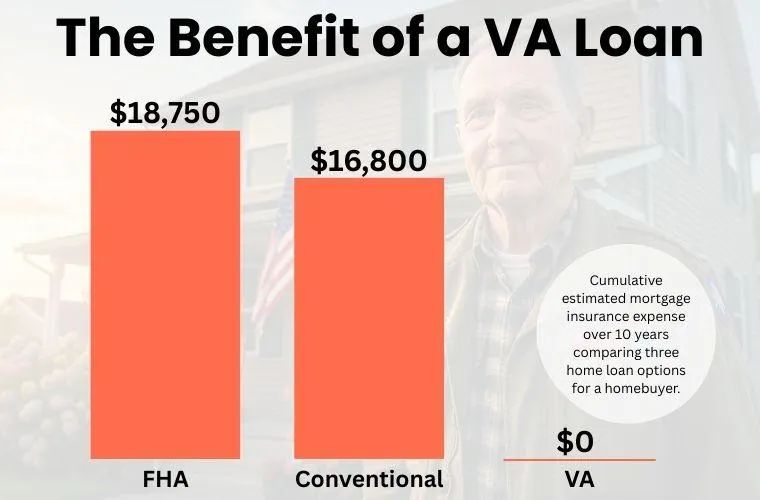

To illustrate the potential costs, here is a graph showing the cumulative mortgage insurance (MI) expense for a conventional loan, an FHA loan, and a VA loan over the course of ten years. The calculations are based on a hypothetical $350,000 home with a 3.5% down payment.

The analysis shows that a VA loan offers the most significant long-term savings by eliminating monthly mortgage insurance.

Mortgage Insurance Comparison

Conventional Loan (PMI): The monthly Private Mortgage Insurance (PMI) is a recurring fee that is typically required when the down payment is less than 20%. In this scenario, the PMI is canceled once the homeowner's equity reaches 20% of the original home value, which happens at approximately month 94. At this point, the monthly PMI payment stops.

FHA Loan (MIP): The FHA loan requires two types of mortgage insurance: a one-time Upfront Mortgage Insurance Premium (UFMIP) and a monthly Annual Mortgage Insurance Premium (MIP). The UFMIP is typically rolled into the loan, increasing the total loan amount. The monthly MIP continues for the entire life of the loan unless the borrower refinances into a conventional loan once they build enough equity.

VA Loan: Eligible veterans and service members can obtain a VA loan, which does not require mortgage insurance. Instead, a one-time VA Funding Fee is charged, which can be paid upfront or financed into the loan. If the veteran has a service connect disability, he / she will be exempt from the funding fee. This is a significant benefit as it removes the burden of a monthly insurance payment.

Veterans who qualify for a VA loan are exempt from mortgage insurance. The Department of Veterans Affairs guarantees the loan which removes the lender’s need to require additional insurance. The result is immediate and ongoing savings. A veteran who might otherwise pay $250, $300, or even $400 per month in mortgage insurance pays nothing under the VA loan program.

Over the life of a mortgage, those savings can add up significantly. Consider a veteran purchasing a $300,000 home with little or no money down. On a conventional loan, PMI could easily cost $200 to $300 per month. Over just five years, that’s $18,000 paid out for insurance that doesn’t build equity and doesn’t reduce principal. The mortgage insurance is simply put in place to protect the financial institution that provides the home loan. Over a period of ten years, the total approaches $36,000. With a VA loan, that money stays in the veteran’s pocket since there is no mortgage insurance.

Lower monthly housing costs for a veteran, or active duty member, can free up income for other goals such as paying down debt, saving for education, investing for retirement, or simply providing more breathing room in a family budget. For veterans transitioning from service into civilian life, that financial flexibility can be invaluable.

We often describe VA loans as the best financing option available in the housing market, and it’s not hard to see why. In addition to eliminating mortgage insurance, VA loans typically offer competitive interest rates and allow for no down payment. Those are two more hurdles that many civilians face when buying a home. The combination of these benefits makes homeownership not only more accessible, but also more sustainable over the long term.

Yet, despite the clear advantages, many veterans never use the benefit. Some assume it’s complicated or just don't explore their VA benefit. Others simply aren’t aware of the savings it provides. Advocates in the housing industry argue that better education is needed to allow veterans to understand what is available to them.

For those who do take advantage, the rewards are substantial. Imagine a veteran homeowner who puts the money saved from mortgage insurance into a retirement account each month. Over time, those contributions, combined with compound growth, could grow into an additional financial cushion worth tens of thousands of dollars by the time they reach retirement.

The VA loan program was created to honor service with opportunity, and in many ways, the elimination of mortgage insurance is its most powerful feature. While it may not be the most visible part of the loan, it’s the one that steadily and silently builds financial strength month after month.

For veterans weighing the choice between renting, buying with a conventional mortgage or using their VA benefit, the numbers speak volumes. Mortgage insurance is a cost civilians can’t avoid without large down payments. Veterans, on the other hand, have already earned the right to bypass it entirely. That difference, played out over years, can mean thousands of dollars saved and invested in their own futures rather than lost to an added fee.

In the end, choosing to use the VA loan isn’t just about securing a roof over one’s head. It’s about unlocking a financial advantage that honors past service with present and future stability. For many veterans, it’s not only the smartest way to buy a home. It's also the path to keeping more of their hard earned money where it belongs.

For more information on the VA loan program, please contact us and we will be happy to assist you.

Mortgage Insight:

Purchasing a Home with a Conventional Loan

VA Loan Success Story with Eric and Denise

How a VA Loan in Ocala, FL changed a Family's Financial Future

How Much Home Can I Afford with a VA Loan?

Can I Use My VA Loan in a Chapter 13 Bankruptcy?

Can a Fiance or Kids be on a VA Loan?

Veterans Who Buy Homes See Far Higher Net Worth Than Renters

How Much Mortgage Insurance Can I Save with a VA Loan?

What to Avoid in a Home When Obtaining a VA Loan Appraisal?

Duplex Property in Fort Lauderdale Quadruples in Value and Leaves a Nest Egg to the Heirs

How a California Remote Worker Obtained a Mortgage to Relocate to Boca Raton, FL

What's the Average Mortgage in Fort Lauderdale, FL?

What Factors are in my Credit Score for a Mortgage?

What Documents Do You Need for a No Income Verification Mortgage?

Restaurant Owner Obtains Self-Employed Home Loan

Can a General Contractor Obtain a No Income Verification Mortgage?

Is a HELOC or a Cash Out Refinance Better to Pay for a New Roof?

Can a Collection Prevent Me from Getting a Mortgage?

Do I Have to Make Mortgage Payments if I Lose My Job?

Your mortgage journey.

Various loan type options including:

Conventional loan

FHA loan

VA loan

Self-employed loan options

No income verification for investors

Benefits of Homeownership

Homeownership is a significant milestone and a decision that offers many advantages. In addition to providing a place to call your own, owning a home brings financial stability, personal fulfillment, and a sense of belonging. Mortgage Group has been helping individuals and families obtain homeownership, guiding them through the process and obtaining referrals to help their family and friends accomplish the same.

Purchase

Get pre-approved to purchase your first home, second home or upcoming investment property.

Refinance

Own a property and interested in lowering your payment? Need to take cash out? Refinance with confidence.

Connect with Us

Our experienced team with be happy to speak with you, and walk you through each step of the process.

Providing mortgage solutions to help you with your home.

Mortgages can be complicated and have many moving parts. Let our team help you!

Contact Us

It only takes a few moments to reach out and have an initial conversation.

Know the Next Steps

Our team will work with you to find the best way to achieve your home loan goals.

Find Your Home and Get Your Loan

Our team will be prepared to move with the next steps once you have secured your home purchase contract.

Houses

Townhomes

Condos

Multi-Units

Read helpful information to assist you with obtaining a mortgage.

Contact our team today.

1-800-583-5305

© Copyright 2026 E Mortgage Capital, Inc.. All rights reserved.

- 1416824 | E Mortgage Capital, Inc.

Notice To Texas Loan Applicants: Consumers wishing to file a complaint against a mortgage banker, or a licensed mortgage banker residential mortgage loan originator, should complete and send a complaint form to the Texas Department of Savings and Mortgage Lending, 2601 North Lamar, Suite 201, Austin, TX 78705. Complaint forms and instructions may be obtained from the department’s website at www.sml.texas.gov

A toll-free consumer hotline is available at 1-877-276-5550. The department maintains a recovery fund to make payments of certain actual out of pocket damages sustained by borrowers caused by acts of licensed mortgage banker residential mortgage loan originators. A written application for reimbursement from the recovery fund must be filed with and investigated by the department prior to the payment of a claim. For more information about the recovery fund, please consult the department’s website at

www.sml.texas.gov