What Portion of a Mortgage Payment Goes Towards Insurance

Learn how this affects the homeowner and even how it can affect the tenant.

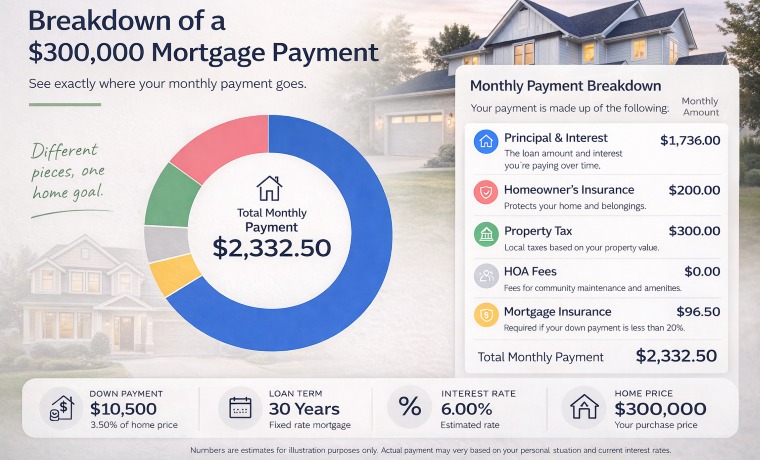

In 2025, homeowners with typical single family mortgages, found themselves paying just under 10% of their monthly mortgage bill not towards principal nor interest, but for the insurance premium alone. That’s a staggering proportion, easily eclipsing what many financial experts laid out as guidelines the past years when it comes to homeownership.

Understanding What’s Fueling the Surge

Homeowners insurance costs have been steadily accelerating. Since early 2020, premiums have climbed roughly 70%, easily outpacing increases in principal, interest, and property taxes, each of which have grown by around 23 to 27% over the same period.

This surge did not happen in a vacuum. A confluence of rising rebuilding costs, escalating risks tied to climate change, an increase in litigation, and higher home valuations have pushed insure companies to raise rates. For example, a 2024 spike of about 14% was followed by forecasted increases of 10% in 2025 and 8% in 2026.

More broadly, between 2020 to 2023, real premiums leapt approximately 20%, and overall since the Great Recession, they’ve soared around 74%, while home prices rose a comparatively moderate 40%, and that's even adjusting for inflation, according to the Harvard Joint Center for Housing Studies.

A Comparison of Two Cities on Opposite Sides of the United States: Tampa Bay and Salt Lake City

National averages tell one part of the story, but regional realities can be especially stark. In Tampa Bay, for example, insurance eats up nearly 14.9% of the average mortgage payment which is well above the national average, driven by consistently high premiums, which have climbed from around $192 to $300 per month over the past decade. Florida homeowners face the highest average annual insurance rates nationwide which were $14,140 in 2024. One in five homeowners opted to go uninsured as a result, according to Axios.

Meanwhile, in Salt Lake City, the climb has been swift. Insurance’s share of mortgage payments has jumped from 4.8% to 6.8% over three years. Monthly insurance payments there have more than doubled, from $61 to $135.

These trends ripple through housing affordability. In Florida, rising insurance costs drag down demand, lengthen time on market, and deter would be buyers. In Salt Lake City, what was once a manageable cost now increasingly strains homeowners’ budgets.

The Hidden Burden for Renters Because You Are Still Paying

Here’s where the narrative becomes especially meaningful for renters. Even if you are not sending money directly to an insurance company, your monthly rent payment likely covers several obligations including your landlord’s insurance, mortgage, property taxes and more.

Studies remind us that homeowners face financial burdens that renters typically avoid: hefty insurance premiums, property taxes, maintenance costs, and more. Homeowners insurance alone averages around $2,400 per year, whereas renters insurance costs are often under $300. When you rent, that hidden cost is baked into what you pay the landlord. But, ultimately, it’s still your money being drawn away from savings or discretionary spending.

Why It All Matters and What You Can Do

Rising insurance costs aren’t just an abstract statistic. They affect real lives and long-term financial planning. Even with mortgage rates easing and overall affordability improving slightly, insurance is squeezing budgets at unprecedented levels.

Moreover, the broader weight of phantom costs which are the additional components of homeownership that inflate overall monthly housing expense beyond the headline mortgage payment is becoming impossible to ignore. Between 2020 to 2025, property insurance alone has increased an estimated 52%, contributing significantly to total monthly housing payments.

In this housing environment, the classic “28% rule” which suggests to keep housing costs under at or under 28% of the gross monthly income has become tougher to reach. While it remains a benchmark by some financial advisors, it may not be realistic for many.

For homeowners, these trends underscore the importance of proactive cost management:

- Shop around for insurance—rates vary widely by insurer and location.

- Raise your deductible if you can afford it which can reduce premiums.

- Bundle policies (e.g., home and auto) to score discounts when it makes sense.

- Invest in mitigation such as security systems, roof upgrades, plumbing improvements, and anything which the insurance provider advises can help lower premiums.

For renters, understanding that part of your rent subsidizes those same rising costs may change your perspective, and become a basis for negotiating lease terms or deciding whether homeownership is worth the trade-offs in your market. This can be especially true if you plan to stay in the same rental or same area for several years. Then, the question must be asked... why rent when you can own? With owning, you can have the ability to build equity.

Today’s homeowners are confronting a landscape where insurance has surged to absorb nearly one in every ten dollars of a mortgage payment. Regional pressures such as Tampa Bay’s near 15%, and Salt Lake City's doubling share hint at wider financial shifts. Meanwhile, renters may already be covering these costs indirectly.

Whether you rent or own, awareness matters as both a tenant and a homeowner. Educate yourself, ask better questions to professionals such as a mortgage broker, and seek out strategies to manage and minimize these burdens. After all, controlling the “hidden” costs of housing is as much a part of financial wellness as the mortgage or rent payment itself.

For more information on no income verification mortgage options, please contact us and we will be happy to assist you.

Mortgage Insight:

Purchasing a Home with a Conventional Loan

VA Loan Success Story with Eric and Denise

How a VA Loan in Ocala, FL changed a Family's Financial Future

Can I Use My VA Loan in a Chapter 13 Bankruptcy?

Can a Fiance or Kids be on a VA Loan?

Veterans Who Buy Homes See Far Higher Net Worth Than Renters

How Much Mortgage Insurance Can I Save with a VA Loan?

What to Avoid in a Home When Obtaining a VA Loan Appraisal?

Duplex Property in Fort Lauderdale Quadruples in Value and Leaves a Nest Egg to the Heirs

How a California Remote Worker Obtained a Mortgage to Relocate to Boca Raton, FL

What's the Average Mortgage in Fort Lauderdale, FL?

What Factors are in my Credit Score for a Mortgage?

What Documents Do You Need for a No Income Verification Mortgage?

Restaurant Owner Obtains Self-Employed Home Loan

Can a General Contractor Obtain a No Income Verification Mortgage?

Is a HELOC or a Cash Out Refinance Better to Pay for a New Roof?

Can a Collection Prevent Me from Getting a Mortgage?

Do I Have to Make Mortgage Payments if I Lose My Job?

How to Rent Out Your Investment Property

What Portion of a Mortgage Payment Goes Towards Insurance

Your mortgage journey.

Various loan type options including:

Conventional loan

FHA loan

VA loan

Self-employed loan options

No income verification for investors

Benefits of Homeownership

Homeownership is a significant milestone and a decision that offers many advantages. In addition to providing a place to call your own, owning a home brings financial stability, personal fulfillment, and a sense of belonging. Mortgage Group has been helping individuals and families obtain homeownership, guiding them through the process and obtaining referrals to help their family and friends accomplish the same.

Purchase

Get pre-approved to purchase your first home, second home or upcoming investment property.

Refinance

Own a property and interested in lowering your payment? Need to take cash out? Refinance with confidence.

Connect with Us

Our experienced team with be happy to speak with you, and walk you through each step of the process.

Providing mortgage solutions to help you with your home.

Mortgages can be complicated and have many moving parts. Let our team help you!

Contact Us

It only takes a few moments to reach out and have an initial conversation.

Know the Next Steps

Our team will work with you to find the best way to achieve your home loan goals.

Find Your Home and Get Your Loan

Our team will be prepared to move with the next steps once you have secured your home purchase contract.

Houses

Townhomes

Condos

Multi-Units

Some of the areas where we have helped individuals obtain a mortgage:

Miami-Dade County

Bal Harbour, FL

Coconut Grove, FL

Coral Gables, FL

Cutler Bay, FL

Eastern Shores, FL

Fisher Island, FL

Golden Beach, FL

Hialeah, FL

Hialeah Gardens, FL

Homestead, FL

Indian Creek, FL

Miami Beach, FL

Miami Gardens, FL

North Miami, FL

North Miami Beach, FL

Pinecrest, FL

Surfside, FL

Broward County

Cooper City, FL

Coral Springs, FL

Dania Beach, FL

Davie, FL

Deerfield Beach, FL

Doral, FL

Fort Lauderdale, FL

Hallandale Beach, FL

Hollywood, FL

Lauderdale by the Sea, FL

Lauderdale Lakes, FL

Lauderhill, FL

Lighthouse Point, FL

Margate, FL

Miramar, FL

North Lauderdale, FL

Oakland Park, FL

Parkland, FL

Pembroke Pines, FL

Plantation, FL

Pompano Beach, FL

Southwest Ranches, FL

Sunrise, FL

Tamarac, FL

West Park, FL

Wilton Manors, FL

How much home can I afford?

Which home loan program is right for me?

Contact our team today.

1-800-583-5305

© Copyright 2026 E Mortgage Capital, Inc.. All rights reserved.

- 1416824 | E Mortgage Capital, Inc.

Notice To Texas Loan Applicants: Consumers wishing to file a complaint against a mortgage banker, or a licensed mortgage banker residential mortgage loan originator, should complete and send a complaint form to the Texas Department of Savings and Mortgage Lending, 2601 North Lamar, Suite 201, Austin, TX 78705. Complaint forms and instructions may be obtained from the department’s website at www.sml.texas.gov

A toll-free consumer hotline is available at 1-877-276-5550. The department maintains a recovery fund to make payments of certain actual out of pocket damages sustained by borrowers caused by acts of licensed mortgage banker residential mortgage loan originators. A written application for reimbursement from the recovery fund must be filed with and investigated by the department prior to the payment of a claim. For more information about the recovery fund, please consult the department’s website at

www.sml.texas.gov