Veterans Who Buy Homes See Far Higher Net Worth Than Renters

According to the Federal Reserve, Homeowners Get Ahead in the Long Run.

For generations, owning a home has been central to the American Dream. For military veterans, it can also be one of the most powerful financial tools available. The latest data confirms what many have long suspected: the wealth gap between homeowners and renters is enormous—and it’s only getting wider.

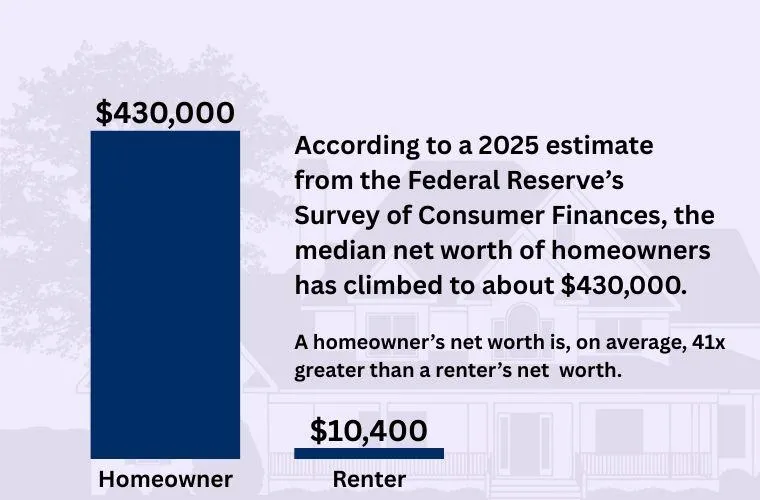

According to a 2025 estimate from the Federal Reserve’s Survey of Consumer Finances, the median net worth of homeowners has climbed to about $430,000. Renters, by comparison, average just $10,000. That means homeowners enjoy a net worth more than forty times greater than those who rent. A 2024 report from the Aspen Institute echoed the same divide, noting that renters possess less than three percent of the wealth of homeowners.

For veterans, this gap presents both a challenge and an opportunity. The Department of Veterans Affairs guarantees VA loans, which allow eligible servicemembers and veterans to purchase a home with no down payment, no private mortgage insurance, and access to competitive interest rates. These benefits remove some of the biggest hurdles to ownership, and can accelerate wealth building in ways that renting never will.

Why Veterans Who Own Get Ahead

When a veteran purchases a home, every monthly mortgage payment contributes to equity. Over time, that ownership stake grows, especially as property values increase. Even modest appreciation, historically averaging around 3 percent annually, according to the Federal Housing Finance Agency, can translate into a six figure boost to a household’s net worth over a decade.

On the other hand, renters watch their housing costs rise year after year without building any equity. Their monthly payments benefit a landlord, not their own financial future. The result is stark and while homeowners accumulate wealth through both equity and appreciation, renters are left with little more than receipts.

For veterans, the VA loan program makes this divide even sharper. Without the need to save for a down payment, veterans can enter the housing market earlier which means they can start building equity while others are still waiting on the sidelines. Over years, that head start can really compound.

A Tale of Two Veterans

Imagine two service members who transition out of the military at the same time. One uses a VA loan to purchase a modest $250,000 home. The other chooses to rent, preferring ease and flexibility, and isn't sure if they want to buy something now.

Ten years later, the first veteran has likely paid down a significant portion of the mortgage while watching the home’s value rise, and potentially adding more than $100,000 to their net worth. The second veteran, despite earning the same paycheck, has far less to show financially.

This is not an abstract exercise. It’s a reflection of what the Federal Reserve’s latest numbers are telling us. Homeownership is the single most significant driver of household wealth in America, and veterans who leverage their benefits are uniquely positioned to take advantage.

The VA Loan Advantage

The Department of Veterans Affairs Annual Benefits Report (2023) documented more than 1.2 million active VA guaranteed loans across the country. Each one represents a veteran or servicemember who has been able to buy without a down payment, avoid the costly burden of private mortgage insurance, and often lock in lower rates than the civilian market.

Over the life of a loan, these advantages can save tens of thousands of dollars. Just as importantly, they reduce barriers to entry, giving veterans a faster pathway into the housing market and, in turn, into wealth creation. Additionally, VA loan eligibility can often be restored after selling a home, meaning the benefit isn’t one and done. It can actually be used multiple times to assist veterans and their families with various home purchases over the course of a lifetime.

More Than Just a Home

Owning a home provides more than financial benefits. For many veterans transitioning into civilian life, a home represents stability, predictability, and a sense of belonging. A fixed rate mortgage keeps monthly housing costs steady, even as rents climb. A home can also serve as collateral for future needs from funding education, helping to pay for retirement, an automobile or even starting a small business.

The financial story remains the most compelling. In 2025, with homeowners now averaging a net worth of $430,000 compared with renters’ $10,000 net worth, the decision to buy or rent is no longer just about lifestyle. It’s about building a future.

The VA Loan Bottom Line

Veterans have already earned the right to use their VA loan benefit. The question is whether they’ll take the step to put it to work. The latest numbers from the Federal Reserve and independent researchers make it clear that veterans who buy homes put themselves on a path to significantly higher net worth than those who rent.

Homeownership is not guaranteed wealth, but for veterans, it is a proven foundation. With the VA loan as a powerful tool, those who served have a chance to turn their sacrifice into long term security and prosperity for themselves, their families and generations to come.

For more information on the VA loan program, please contact us and we will be happy to assist you.

Mortgage Insight:

Purchasing a Home with a Conventional Loan

VA Loan Success Story with Eric and Denise

How a VA Loan in Ocala, FL changed a Family's Financial Future

Can I Use My VA Loan in a Chapter 13 Bankruptcy?

Can a Fiance or Kids be on a VA Loan?

Veterans Who Buy Homes See Far Higher Net Worth Than Renters

How Much Mortgage Insurance Can I Save with a VA Loan?

What to Avoid in a Home When Obtaining a VA Loan Appraisal?

Duplex Property in Fort Lauderdale Quadruples in Value and Leaves a Nest Egg to the Heirs

How a California Remote Worker Obtained a Mortgage to Relocate to Boca Raton, FL

What's the Average Mortgage in Fort Lauderdale, FL?

What Factors are in my Credit Score for a Mortgage?

What Documents Do You Need for a No Income Verification Mortgage?

Restaurant Owner Obtains Self-Employed Home Loan

Can a General Contractor Obtain a No Income Verification Mortgage?

Is a HELOC or a Cash Out Refinance Better to Pay for a New Roof?

Can a Collection Prevent Me from Getting a Mortgage?

Do I Have to Make Mortgage Payments if I Lose My Job?

Your mortgage journey.

Various loan type options including:

Conventional loan

FHA loan

VA loan

Self-employed loan options

No income verification for investors

Benefits of Homeownership

Homeownership is a significant milestone and a decision that offers many advantages. In addition to providing a place to call your own, owning a home brings financial stability, personal fulfillment, and a sense of belonging. Mortgage Group has been helping individuals and families obtain homeownership, guiding them through the process and obtaining referrals to help their family and friends accomplish the same.

Purchase

Get pre-approved to purchase your first home, second home or upcoming investment property.

Refinance

Own a property and interested in lowering your payment? Need to take cash out? Refinance with confidence.

Connect with Us

Our experienced team with be happy to speak with you, and walk you through each step of the process.

Providing mortgage solutions to help you with your home.

Mortgages can be complicated and have many moving parts. Let our team help you!

Contact Us

It only takes a few moments to reach out and have an initial conversation.

Know the Next Steps

Our team will work with you to find the best way to achieve your home loan goals.

Find Your Home and Get Your Loan

Our team will be prepared to move with the next steps once you have secured your home purchase contract.

Houses

Townhomes

Condos

Multi-Units

Some of the areas where we have helped individuals obtain a mortgage:

Miami-Dade County

Bal Harbour, FL

Coconut Grove, FL

Coral Gables, FL

Cutler Bay, FL

Eastern Shores, FL

Fisher Island, FL

Golden Beach, FL

Hialeah, FL

Hialeah Gardens, FL

Homestead, FL

Indian Creek, FL

Miami Beach, FL

Miami Gardens, FL

North Miami, FL

North Miami Beach, FL

Pinecrest, FL

Surfside, FL

Broward County

Cooper City, FL

Coral Springs, FL

Dania Beach, FL

Davie, FL

Deerfield Beach, FL

Doral, FL

Fort Lauderdale, FL

Hallandale Beach, FL

Hollywood, FL

Lauderdale by the Sea, FL

Lauderdale Lakes, FL

Lauderhill, FL

Lighthouse Point, FL

Margate, FL

Miramar, FL

North Lauderdale, FL

Oakland Park, FL

Parkland, FL

Pembroke Pines, FL

Plantation, FL

Pompano Beach, FL

Southwest Ranches, FL

Sunrise, FL

Tamarac, FL

West Park, FL

Wilton Manors, FL

How much home can I afford?

Which home loan program is right for me?

Contact our team today.

1-800-583-5305

© Copyright 2026 E Mortgage Capital, Inc.. All rights reserved.

- 1416824 | E Mortgage Capital, Inc.

Notice To Texas Loan Applicants: Consumers wishing to file a complaint against a mortgage banker, or a licensed mortgage banker residential mortgage loan originator, should complete and send a complaint form to the Texas Department of Savings and Mortgage Lending, 2601 North Lamar, Suite 201, Austin, TX 78705. Complaint forms and instructions may be obtained from the department’s website at www.sml.texas.gov

A toll-free consumer hotline is available at 1-877-276-5550. The department maintains a recovery fund to make payments of certain actual out of pocket damages sustained by borrowers caused by acts of licensed mortgage banker residential mortgage loan originators. A written application for reimbursement from the recovery fund must be filed with and investigated by the department prior to the payment of a claim. For more information about the recovery fund, please consult the department’s website at

www.sml.texas.gov