Can Refinancing Your Car Help You Qualify for a Mortgage?

Understand how your vehicle payment can effect your debt to income ratio.

If you are planning to buy a home, you have probably heard that your finances will be put under a microscope during the mortgage approval process. An underwriter will look at your income, credit score, assets and existing debts to determine whether you qualify for a home loan and how much you can borrow.

One debt that often gets overlooked is your auto loan. While a car payment may seem unrelated to buying a home, it can have a significant impact on your mortgage application. In some cases, refinancing your car loan before applying for a mortgage could improve your financial profile and increase your chances of approval.

But is refinancing your vehicle always the right move? Let's take a closer look at how auto loan refinancing can affect mortgage qualification and what homebuyers should consider before making a decision.

How an Underwriter Evaluates Your Finances

When reviewing a mortgage application, an underwriter can focus on several key factors such as credit score, income and employment history, savings and assets, debt to income ratio (DTI) and payment history. Of these factors, your debt to income ratio is often one of the most important.

Your DTI compares your monthly debt obligations to your gross monthly income. It helps lenders determine whether you'll be able to comfortably manage a mortgage payment in addition to your existing financial commitments.

For example, if you earn $6,000 per month before taxes and have $2,100 in monthly debt payments including the upcoming housing payment, your DTI would be 35%..

The lower your DTI, the better it can be for underwriting. The reality is that for many individuals, the DTI can be higher and working with your mortgage specialist can be crucial in determining what can be done to help reduce the liabilities.

Qualifying for a mortgage involves more than just your credit score. Lenders evaluate your overall financial picture to determine how much home you can afford and your likelihood of successful repayment.

Your financial profile plays a key role in mortgage approval. Strong credit, stable income, manageable debt, and consistent payment history can improve your chances of qualifying for favorable loan terms.

Why Your Car Payment Matters

Many borrowers are surprised to learn that their car payment can directly affect how much home they can afford.

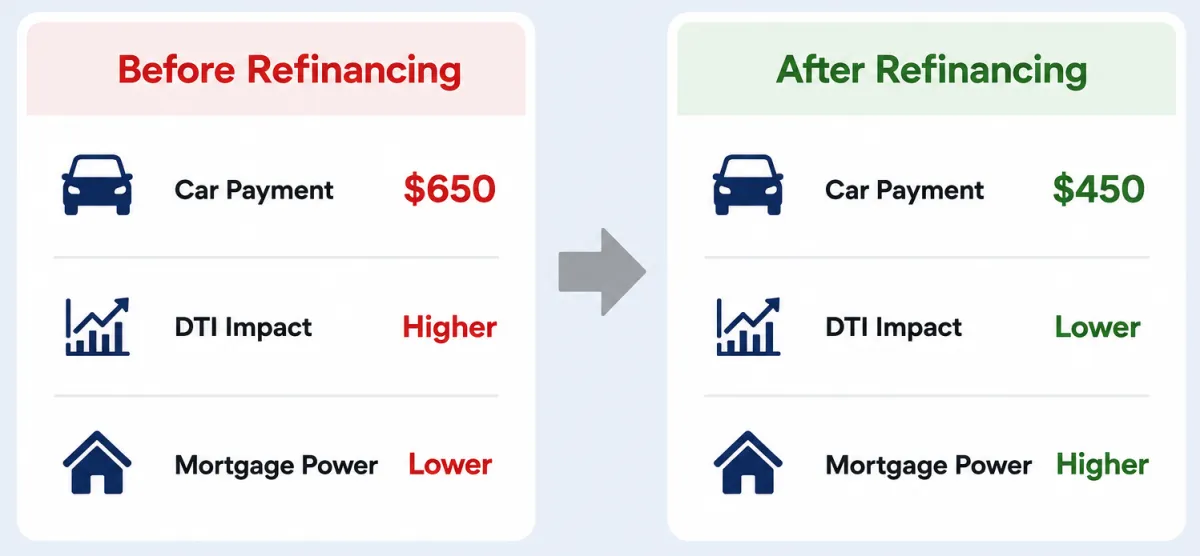

Let's suppose your monthly auto loan payment is $650. That payment is included in your DTI calculation, along with credit cards, student loans, personal loans, and other recurring obligations.

If your debt payments are already close to a lender's maximum threshold, a large auto loan payment could reduce the mortgage amount you qualify for—or even prevent approval altogether.

This is where refinancing may come into play.

How Refinancing Your Car Could Help

Auto loan refinancing involves replacing your current vehicle loan with a new one, ideally with more favorable terms.

Depending on your situation, refinancing may help by lowering your monthly payments, improving cash flow and potentially strengthening your credit profile.

Lowering Your Monthly Payment

One of the most common reasons people refinance a vehicle is to reduce their monthly payment.

Interest rates have dropped

Your credit score has improved

You extend the loan term

You qualify for better financing terms

A lower monthly payment can reduce your DTI ratio, potentially making it easier to qualify for a mortgage.

For example, if refinancing lowers your car payment from $650 to $450 per month, that's $200 less debt counted against you each month. That reduction may improve your mortgage eligibility and increase your purchasing power.

Improving Cash Flow

Mortgage lenders want to see that borrowers have enough financial flexibility to handle homeownership expenses.

Lowering your car payment may free up additional cash each monthly for

Mortgage payments

Property taxes

Homeowners insurance

Emergency savings

Closing costs

Strong cash flow can make your overall financial profile more attractive.

Potentially Strengthening Your Credit Profile

In some cases, refinancing may also help borrowers improve their credit situation.

If refinancing allows you to make payments more comfortably and avoid late payments, your credit score may benefit over time.

A stronger credit score can help you qualify for better mortgage rates and loan programs.

When Refinancing May Not Help

While refinancing can be beneficial, it's not always the best solution.

Extending the Loan Term

Many borrowers lower their monthly payment by stretching the loan over a longer period.

While this may improve DTI, it often means paying more interest over the life of the loan.

For example, reducing your payment by extending a loan from three years to six years may help your mortgage application today, but it could cost thousands of dollars in additional interest over time.

It's important to weigh both the short-term and long-term financial impact.

Creating a New Credit Inquiry

When you refinance a vehicle, lenders typically perform a hard credit inquiry.

While the effect is usually small and temporary, any credit activity before a mortgage application should be considered carefully.

If you're planning to apply for a mortgage within the next few weeks, it may be wise to discuss the timing with your mortgage professional before refinancing.

Increasing Total Debt Costs

A lower payment doesn't always mean a better loan.

Some borrowers refinance into loans that reduce monthly obligations but increase total borrowing costs.

Mortgage lenders may focus primarily on your monthly payment, but your overall financial health matters too.

Timing Matters

If you're considering refinancing your car before buying a home, timing can be important.

Generally speaking, making major financial changes right before applying for a mortgage can complicate the underwriting process.

Other Ways to Improve Mortgage Qualification

Refinancing your auto loan is only one potential strategy.

Homebuyers may also improve their mortgage eligibility by:

Paying Down Credit Card Balances

Credit card debt often has a greater impact on mortgage qualification than borrowers realize.

Reducing revolving debt can improve both DTI and credit scores.

Avoiding New Debt

Taking on additional loans before applying for a mortgage can reduce purchasing power and create underwriting challenges.

Many mortgage professionals recommend postponing major purchases until after closing.

Increasing Income

A higher income can improve your debt-to-income ratio and potentially qualify you for a larger mortgage amount.

Building Savings

Lenders generally like to see financial reserves. Having money available for a down payment, closing costs, and emergencies can strengthen your application.

Should You Refinance Your Car Before Applying for a Mortgage?

The answer depends on your individual financial situation.

Refinancing your car may help if:

It significantly lowers your monthly payment

It improves your debt-to-income ratio

It creates better cash flow

The long-term costs make financial sense

However, refinancing may not be beneficial if:

The savings are minimal

The loan term becomes excessively long

You are only weeks away from applying for a mortgage

The refinance creates unnecessary financial complications

The best approach is to look at your complete financial picture rather than focusing on a single debt.

A car loan may seem unrelated to buying a home, but it can play an important role in the mortgage approval process. As auto loan payments are included in your debt to income ratio, refinancing your vehicle could potentially improve your ability to qualify for a mortgage by lowering your monthly obligations and increasing financial flexibility.

With that said, refinancing isn't a one size fits all solution. The benefits depend on factors such as your current loan terms, credit profile, homebuying timeline and overall financial goals.

If you are planning to purchase a home in the near future, speaking with a mortgage specialist can help you determine whether refinancing your vehicle is a smart move, or whether there are other strategies that may have a greater impact on your mortgage approval and homebuying power.

Getting Pre-Approved

If you are ready to take the next step and get pre-approved to purchase a home or possibly refinance an existing home, please contact us. Our professional staff will look forward to speaking with you.

Mortgage Insight:

Purchasing a Home with a Conventional Loan

VA Loan Success Story with Eric and Denise

How a VA Loan in Ocala, FL changed a Family's Financial Future

Can I Use My VA Loan in a Chapter 13 Bankruptcy?

Can a Fiance or Kids be on a VA Loan?

Veterans Who Buy Homes See Far Higher Net Worth Than Renters

How Much Mortgage Insurance Can I Save with a VA Loan?

Duplex Property in Fort Lauderdale Quadruples in Value and Leaves a Nest Egg to the Heirs

How a California Remote Worker Obtained a Mortgage to Relocate to Boca Raton, FL

What's the Average Mortgage in Fort Lauderdale, FL?

What Factors are in my Credit Score for a Mortgage?

What Documents Do You Need for a No Income Verification Mortgage?

Restaurant Owner Obtains Self-Employed Home Loan

Can a General Contractor Obtain a No Income Verification Mortgage?

Is a HELOC or a Cash Out Refinance Better to Pay for a New Roof?

Can a Collection Prevent Me from Getting a Mortgage?

Do I Have to Make Mortgage Payments if I Lose My Job?

How to Rent Out Your Investment Property

How Private Money Works in Real Estate Investing

What Portion of a Mortgage Payment Goes Towards Insurance

How Much Cash Can I Take Out of My Home?

Top 5 Purposes for a Cash-Out Refinance

Is My VA Disability Income Enough for a VA Loan?

Can I Use a VA Loan More Than One Time?

Helping Renters Build Credit with These 4 Strategies

How to Get a Mortgage Pre-Approval Letter

What Fannie Mae’s Crypto Move Means for Homebuyers?

How Business Owners Can Qualify for an Interest Only Home Loan?

Your mortgage journey.

Various loan type options including:

Conventional loan

FHA loan

VA loan

Self-employed loan options

No income verification for investors

Benefits of Homeownership

Homeownership is a significant milestone and a decision that offers many advantages. In addition to providing a place to call your own, owning a home brings financial stability, personal fulfillment, and a sense of belonging. Mortgage Group has been helping individuals and families obtain homeownership, guiding them through the process and obtaining referrals to help their family and friends accomplish the same.

Purchase

Get pre-approved to purchase your first home, second home or upcoming investment property.

Refinance

Own a property and interested in lowering your payment? Need to take cash out? Refinance with confidence.

Connect with Us

Our experienced team with be happy to speak with you, and walk you through each step of the process.

Providing mortgage solutions to help you with your home.

Mortgages can be complicated and have many moving parts. Let our team help you!

Contact Us

It only takes a few moments to reach out and have an initial conversation.

Know the Next Steps

Our team will work with you to find the best way to achieve your home loan goals.

Find Your Home and Get Your Loan

Our team will be prepared to move with the next steps once you have secured your home purchase contract.

Houses

Townhomes

Condos

Multi-Units

Contact our team today.

1-800-583-5305

© Copyright 2026 E Mortgage Capital, Inc.. All rights reserved.

- 1416824 | E Mortgage Capital, Inc.

Notice To Texas Loan Applicants: Consumers wishing to file a complaint against a mortgage banker, or a licensed mortgage banker residential mortgage loan originator, should complete and send a complaint form to the Texas Department of Savings and Mortgage Lending, 2601 North Lamar, Suite 201, Austin, TX 78705. Complaint forms and instructions may be obtained from the department’s website at www.sml.texas.gov

A toll-free consumer hotline is available at 1-877-276-5550. The department maintains a recovery fund to make payments of certain actual out of pocket damages sustained by borrowers caused by acts of licensed mortgage banker residential mortgage loan originators. A written application for reimbursement from the recovery fund must be filed with and investigated by the department prior to the payment of a claim. For more information about the recovery fund, please consult the department’s website at

www.sml.texas.gov