How Business Owners Can Qualify for an Interest Only Home Loan?

See if an interest only mortgage is the right choice for you as a self-employed borrower.

For many business owners, cash flow is one of the most important aspects of financial management. Whether you are reinvesting profits into your company, hiring employees, purchasing equipment, or preparing for future growth maintaining liquidity can be critical to your success.

That's one reason many entrepreneurs explore interest only home loans when purchasing or refinancing a property. An interest only home loan can offer lower monthly payments during the initial years of the loan, allowing business owners to preserve more cash for their business and other investments.

But, can a business owner actually qualify for an interest only mortgage?

The answer is yes. We offer interest only home loan programs specifically designed for self-employed borrowers and business owners. However, qualification requirements are often different from those of traditional mortgages.

What Is an Interest Only Home Loan?

An interest-only mortgage allows borrowers to pay only the interest portion of the loan for a predetermined period, typically around ten years. During this time, monthly payments are lower because the loan balance itself is not being reduced.

Once the interest-only period ends, the borrower begins making payments toward both principal and interest. As a result, monthly payments generally increase after the initial period expires.

For business owners, this structure can provide valuable financial flexibility during the early years of the loan.

Why Business Owners May Choose Interest Only Financing

Traditional mortgage payments can tie up a significant amount of monthly cash flow. For entrepreneurs, that money may be better utilized elsewhere.

An interest only loan may help business owners:

For someone whose business is growing rapidly, having access to additional cash each month can create opportunities that may generate returns far greater than the cost of the mortgage.

Who Typically Qualifies for an Interest Only Home Loan?

While every lender has its own guidelines, interest only mortgages are generally designed for financially strong borrowers. Business owners who qualify often share several characteristics:

The stronger these factors are, the higher probability of qualifying for an interest only mortgage.

Business Ownership History Matters

One of the first things an underwriter will review is how long you have been in business.

In most cases, borrowers should have owned and operated their business for at least two years. This operating history helps demonstrate stability and reduces the perceived risk associated with self-employment income.

Businesses that have been operating successfully for several years often have a stronger track record of generating revenue and weathering economic fluctuations. The longer and more stable the business history, the more confidence lenders generally have in the borrower's ability to repay the loan.

If you have been self-employed for less than two years, qualifying may still be possible in certain situations, but options may be more limited.

Good to Excellent Credit Is Typically Required

Credit quality plays a major role in qualifying for an interest only home loan.

As these loans carry additional risk compared to traditional fully amortized mortgages, underwriters often look for borrowers with strong credit profiles.

A good to excellent credit score demonstrates responsible financial management and a history of making payments on time. If your credit profile has room for improvement, paying down outstanding debts and correcting any reporting errors before applying can help strengthen your application.

Cash Flow Is Often More Important Than Tax Returns

One of the biggest misconceptions among business owners is that they must show substantial income on their tax returns to qualify for a mortgage. In reality, many successful business owners use legitimate tax strategies, deductions, and write offs that reduce their taxable income. While this can be beneficial from a tax perspective, it sometimes creates challenges when applying for traditional financing.

Fortunately, we offer various interest only loan programs that recognize this reality.

Rather than focusing exclusively on tax returns, an underwriter will often evaluate the overall cash flow of the business. Their primary concern is whether the business generates enough income to comfortably support the mortgage payment. To assess cash flow, we will often request.

The goal is to determine whether the business has the financial capacity to support the loan, regardless of how much taxable income appears on a tax return.

For many entrepreneurs, this approach provides a more accurate picture of their true financial strength.

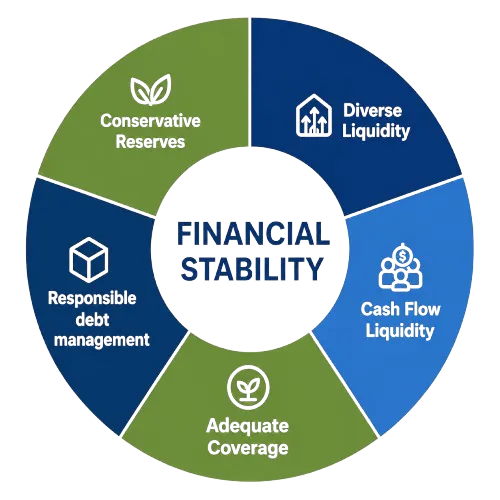

Demonstrating Financial Stability

In addition to strong cash flow, an underwriter will want to see evidence of overall financial stability. An underwriter will understand that business income can fluctuate from month to month. What matters most is demonstrating that your business generates sufficient cash flow over time and that you have the resources to manage your financial obligations.

The Importance of Cash Reserves

Many underwriters prefer borrowers to have additional funds available after closing. Cash reserves provide reassurance that you can continue making mortgage payments if business revenue temporarily declines or unexpected expenses arise.

Depending on the loan program, reserves may include:

Having substantial reserves can significantly strengthen an application and may improve approval odds.

Is an Interest Only Mortgage Right for You?

An interest only home loan can be an excellent option for business owners who prioritize cash flow and financial flexibility. However, it is important to understand how the loan works and prepare for the eventual transition to principal and interest payments. Some business owners plan to only keep the loan for a few years because they may consider selling the property, refinancing the loan or paying it off altogether in a few years.

Before applying, consider:

Your long income expectations

Future business growth plan

Available cash reserves

Ability to handle higher payments later

Overall financial objectives

Exit strategy (refinance, sell, or payoff)

For many established business owners, the benefits of preserving capital and maintaining liquidity can outweigh the drawbacks.

Business owners can absolutely qualify for an interest only home loan, especially when they have a strong financial foundation. In most cases, we want to ensure the borrower has had the business for at least two years, maintains strong credit and can demonstrate consistent cash flow in their company.

Unlike traditional mortgage programs that may rely heavily on tax returns, many of our interest only loan options focus on the overall financial health of your company and its ability to support the proposed mortgage payment.

If your business generates strong cash flow, you have established a solid operating history, and you maintain healthy credit, an interest only mortgage may provide the flexibility needed to preserve capital while continuing to grow your business.

Contact our team to inquire about an interest only mortgage, or other mortgage options, for your scenario.

Mortgage Insight:

Purchasing a Home with a Conventional Loan

VA Loan Success Story with Eric and Denise

How a VA Loan in Ocala, FL changed a Family's Financial Future

Can I Use My VA Loan in a Chapter 13 Bankruptcy?

Can a Fiance or Kids be on a VA Loan?

Veterans Who Buy Homes See Far Higher Net Worth Than Renters

How Much Mortgage Insurance Can I Save with a VA Loan?

Duplex Property in Fort Lauderdale Quadruples in Value and Leaves a Nest Egg to the Heirs

How a California Remote Worker Obtained a Mortgage to Relocate to Boca Raton, FL

What's the Average Mortgage in Fort Lauderdale, FL?

What Factors are in my Credit Score for a Mortgage?

What Documents Do You Need for a No Income Verification Mortgage?

Restaurant Owner Obtains Self-Employed Home Loan

Can a General Contractor Obtain a No Income Verification Mortgage?

Is a HELOC or a Cash Out Refinance Better to Pay for a New Roof?

Can a Collection Prevent Me from Getting a Mortgage?

Do I Have to Make Mortgage Payments if I Lose My Job?

How to Rent Out Your Investment Property

How Private Money Works in Real Estate Investing

What Portion of a Mortgage Payment Goes Towards Insurance

How Much Cash Can I Take Out of My Home?

Top 5 Purposes for a Cash-Out Refinance

Is My VA Disability Income Enough for a VA Loan?

Can I Use a VA Loan More Than One Time?

Helping Renters Build Credit with These 4 Strategies

How to Get a Mortgage Pre-Approval Letter

What Fannie Mae’s Crypto Move Means for Homebuyers?

Can a Canadian Citizen Get a U.S. Mortgage?

Your mortgage journey.

Various loan type options including:

Conventional loan

FHA loan

VA loan

Self-employed loan options

No income verification for investors

Benefits of Homeownership

Homeownership is a significant milestone and a decision that offers many advantages. In addition to providing a place to call your own, owning a home brings financial stability, personal fulfillment, and a sense of belonging. Mortgage Group has been helping individuals and families obtain homeownership, guiding them through the process and obtaining referrals to help their family and friends accomplish the same.

Purchase

Get pre-approved to purchase your first home, second home or upcoming investment property.

Refinance

Own a property and interested in lowering your payment? Need to take cash out? Refinance with confidence.

Connect with Us

Our experienced team with be happy to speak with you, and walk you through each step of the process.

Providing mortgage solutions to help you with your home.

Mortgages can be complicated and have many moving parts. Let our team help you!

Contact Us

It only takes a few moments to reach out and have an initial conversation.

Know the Next Steps

Our team will work with you to find the best way to achieve your home loan goals.

Find Your Home and Get Your Loan

Our team will be prepared to move with the next steps once you have secured your home purchase contract.

Houses

Townhomes

Condos

Multi-Units

Contact our team today.

1-800-583-5305

© Copyright 2026 E Mortgage Capital, Inc.. All rights reserved.

- 1416824 | E Mortgage Capital, Inc.

Notice To Texas Loan Applicants: Consumers wishing to file a complaint against a mortgage banker, or a licensed mortgage banker residential mortgage loan originator, should complete and send a complaint form to the Texas Department of Savings and Mortgage Lending, 2601 North Lamar, Suite 201, Austin, TX 78705. Complaint forms and instructions may be obtained from the department’s website at www.sml.texas.gov

A toll-free consumer hotline is available at 1-877-276-5550. The department maintains a recovery fund to make payments of certain actual out of pocket damages sustained by borrowers caused by acts of licensed mortgage banker residential mortgage loan originators. A written application for reimbursement from the recovery fund must be filed with and investigated by the department prior to the payment of a claim. For more information about the recovery fund, please consult the department’s website at

www.sml.texas.gov